[阅读中文版本]

Most people in local market had heard a statement similar to this:

"The daily move of KL market is affected by US. If US market rise during the previous night then most probably KLCI will rise today."

People that believe in it may watch the US market throughout the night, and hope to get some idea to trade in the following day.

Well, if you'd ever tried to use the statement to form a day-trade strategy, you'll probably quite upset with it. While it seems to be correct from statistical view, you just can't make money from it.

Why?

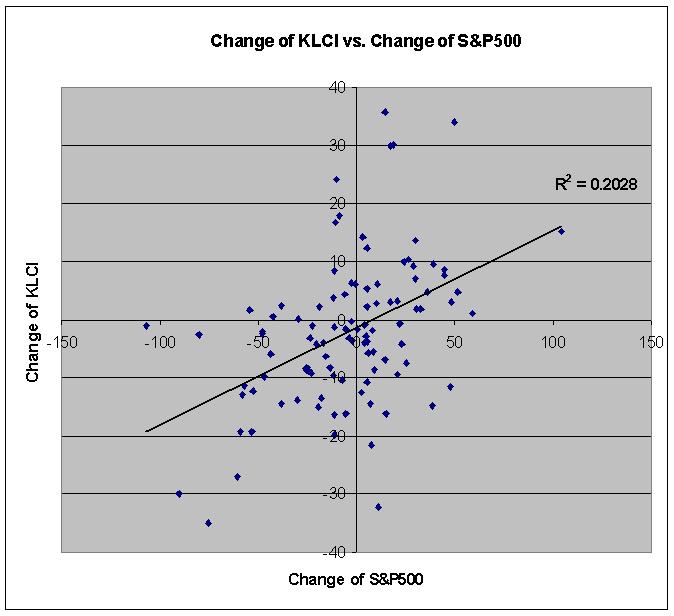

Before we continue, let's look at some historical data. The following chart shows daily relationship between local market and US market. Each point indicate the change of KLCI on a certain day, and the change of S&P500 index the night before. (I only plot about 100 data in this chart, so that it won't be too populated.)

From the chart, we can see that there's a weak relationship between local & US market (correlation coeficient ~ 0.45). So, we can say that the above statement is correct -- if US market rise, our market most probably will follow too.

Then why we can't make a profit out of it?

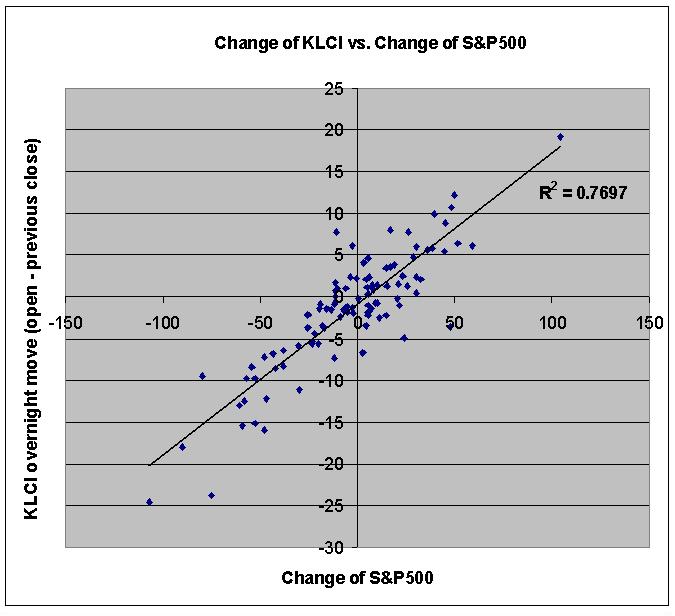

We can see the reason if we divide the change of KLCI in each day into two components:

- The difference between opening price and the previous close.

- the following move in that day. (closing price - opening price)

The sum of these two components equals the daily change of KLCI as comparing to previous close. We examine them one by one. First, we check the the relationship of the first component (opening price - previous close) with US market:

As you see, there is a strong relationship between them. So, when US market rise in a particular night, our market most probably will "open high" in the next morning. If Us market drop, KLCI will "open low". Our market's opening price is strongly affected by US.

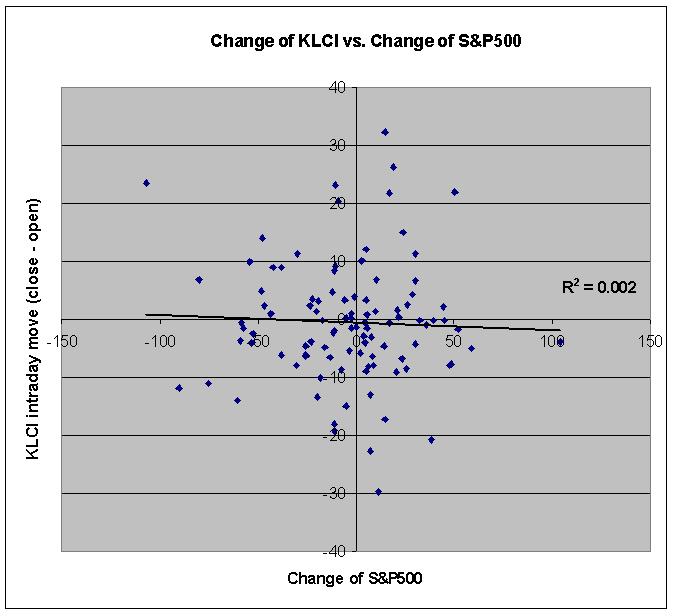

What happen after the market open?

Here come the second component. The following chart relate the moves of KLCI within a day to the S&P500 index change in previous night. It's very clear that after the market open, the following move within the day is totally unrelated to US market.

Conclusion:

When US market rise during the night, it will immediately reflect in our market with a higher opening price in the morning. After opening, the move of our market is totally independent. So, you can never make money by simply watching US market throughout the night unless you can trade KLCI at a favorable price before it open.

The statement quoted in the beginning of this article -- just like other statements made by most economist --

it is true, but useless !