In early July, this company came into my sight when I was browsing through the postings in Investalks Forum.

Once I saw it, my eyes just can't move away from its unbelievable low price -- a PE as low as 2!

After several days of study and collecting information, I found that its financial situation and growth potential is great. Then, I decided to buy it at 36.5sen.

Here's some attractive numbers of XDL:

- ROE ~ 40%。

- Debt/Equity = 0.24.

- During years 2006 ~ 2009: Revenue CAGR = 59%, profit CAGR = 79%.

The numbers are great, yet it was trading at a price of PE=2, sounds not logical...

I had gone through its IPO prospectus, annual reports, also browse through some blogs and forums, and search for any information available on the internet. Finally came to my own conclusion about its extremely low price -- these newly listed China company just can't get confidence from the public! No matter how good is the data, people just don't believe in it. Manny worrying that it's another conman company.

I don't have a strong confidence in XDL either. But my thought was simple -- Since I didn't see any suspicious point in the data, I choose to believe it. But, isn't it too risky? ... Yes, it's risky -- if you put 50% of your fund in it. For me, I just invested RM5k+ , i.e. just about 10% of my entire portfolio value. I feel quite comfortable with this.

I think I will hold on to this stock for several years, as long as its fundamental remain strong.

.

x x x

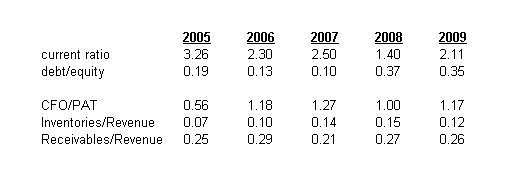

The following spreadsheet shows some data that I sort out from XDL's IPO prospectus and annual report.

(NOTE: Currently there are 3 subsidiaries under XDL. They were separated entities before the listing. Its IPO prospectus only provides separated balance sheets data for these three entities. The consolidated data below is from my own calculation -- I sum up their numbers, then eliminate the related-parties & inter-companies' borrowings/receivables. There will be some errors in the calculation, which is unavoidable, due to the limited information disclosed.)

I had put the data on Google-Docs (click here to see the complete spreadsheet) for easier sharing. I will continuously updating the data in the future.

.