Got to know this company recently through an investment forum.

I like this company very much after doing some research... It got so many criteria that I'm looking for, and no doubt a candidate of long-term growth stocks.

CBIP is a leader in its niche market -- construction and engineering of palm oil mills. The company had been in this business for more than three decades, and had built a very strong customer base... Felda, Wilmar, Sime Darby, TradeWinds Plantation, etc., are among its customers. One of its main product, Modipalm Continuous Sterilization System, is patented in Malaysia and Indonesia till 2021.

One thing I like very much regarding the core business of CBIP -- it's relatively less impacted by the fluctuation of CPO price. Its customers (the palm oil plantation companies) effectively act as a buffer between CBIP and palm-oil market... So, investing in CBIP is like enjoying a piece of pie from the huge palm-oil economics, without taking the risk of CPO price plunge...

Besides these, CBIP had been doing business in retrofitting of special purpose vehicles. It also had associated and JV which involves in palm-oil plantation. Currently the contributions from this two segment are relatively small. However, the profit from associates and JV could leap high if the CPO price rebound.

x x x

Ten-years financial performance: (full view here)

Highlights:

x x x

Short-term prospect:

Resulted from the high CPO price during past few years, currently we are experiencing a boom of new palm-oil estate, especially in Indonesia... during these years, we saw new players entering palm-plantation business, while existing players developing new estate... So, in the next 3~5 years, there will be huge demand on palm-oil-mills constructions to absorbs all these new FFB production.

The momentum of this palm-estate expansion wave in Indonesia is going to last for few years even if the CPO price remain low... so I'm seeing a strong sustainable growth on CBIP's core business, and expecting a CAGR of >20% in the next five years.

x x x

Long-term prospect.

I like this company very much after doing some research... It got so many criteria that I'm looking for, and no doubt a candidate of long-term growth stocks.

CBIP is a leader in its niche market -- construction and engineering of palm oil mills. The company had been in this business for more than three decades, and had built a very strong customer base... Felda, Wilmar, Sime Darby, TradeWinds Plantation, etc., are among its customers. One of its main product, Modipalm Continuous Sterilization System, is patented in Malaysia and Indonesia till 2021.

One thing I like very much regarding the core business of CBIP -- it's relatively less impacted by the fluctuation of CPO price. Its customers (the palm oil plantation companies) effectively act as a buffer between CBIP and palm-oil market... So, investing in CBIP is like enjoying a piece of pie from the huge palm-oil economics, without taking the risk of CPO price plunge...

Besides these, CBIP had been doing business in retrofitting of special purpose vehicles. It also had associated and JV which involves in palm-oil plantation. Currently the contributions from this two segment are relatively small. However, the profit from associates and JV could leap high if the CPO price rebound.

x x x

Ten-years financial performance: (full view here)

* Revenue and profit for FY2011 & 2012 are excluding the discontinued plantation business and one-off gain from disposal of subsidiaries.

Highlights:

- Strong consistent growth record -- 16% CAGR for revenue and 24% CAGR of profit during past ten years.

- High ROE -- 22% (ten year average), and it's quite consistent.

- Good profit margin, and it show a gradually improving trend over years.

x x x

Short-term prospect:

Resulted from the high CPO price during past few years, currently we are experiencing a boom of new palm-oil estate, especially in Indonesia... during these years, we saw new players entering palm-plantation business, while existing players developing new estate... So, in the next 3~5 years, there will be huge demand on palm-oil-mills constructions to absorbs all these new FFB production.

The momentum of this palm-estate expansion wave in Indonesia is going to last for few years even if the CPO price remain low... so I'm seeing a strong sustainable growth on CBIP's core business, and expecting a CAGR of >20% in the next five years.

x x x

Long-term prospect.

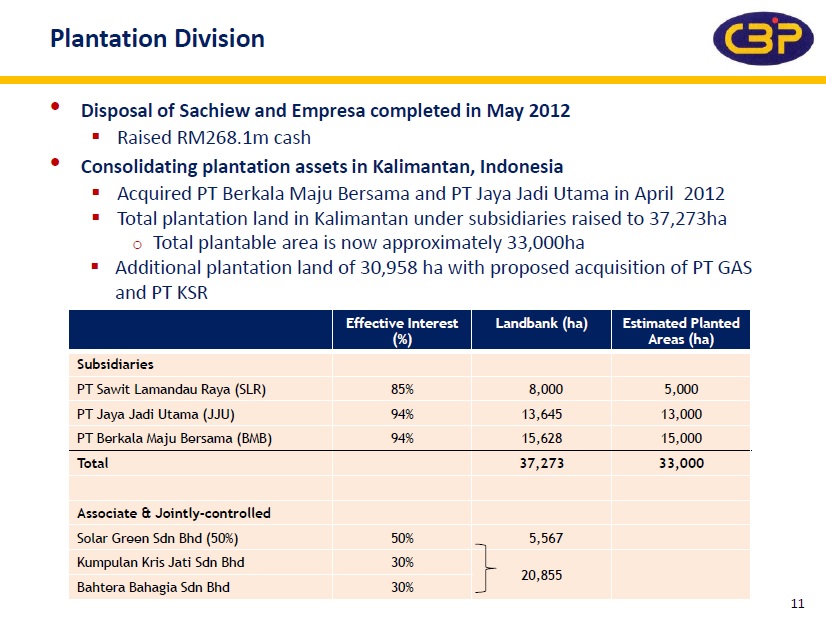

CBIP had been buying plantation lands in Indonesia recently... Currently it already accumulate ~30k ha of landbank, and the figure will jump to 60k ha upon the completion of another two acquisition.

In the next few years, the company will plant these lands with oil-palm, and construct CPO mills in the estates. We will see the contribution from these estates on ~2018 onwards...

When the estates come to mature and start production, they will transform the company into a medium size palm-oil players, and CBIP will going to experience another leap of revenue and profit... maybe 20% CAGR for another 5~10 years?

The land banks of CBIP and its planting plans:(source: CBIP Investor Relation.)

There's a possibility that CBIP won't seriously venture

into plantation segment, but instead sell all those estates when they come

into mature. (like what it did to two of its subsidiaries recently)... If this happen, then we will see a round of huge one-off profit in

its income statement... good news for shareholders though...

x x x

My Investment:

The company posses an EPS of ~32sen for FY2012... I bought the shares at RM2.88, which is equivalent to ~9x PE, a quite reasonable price I think.

Past records show that pay-out ratio of the company was quite low (exception on 2012, when the company received huge cash from the disposal of plantation subsidiaries). Hence I didn't expect much from its dividend yield...

Expected term of investment: five years, hopefully would be longer.

Expected return: 20% p.a., mainly from stock price gain.

x x x

The investment in CBIP made up ~7.5% of my fund... Combine with TSH, the palm-oil related companies now weigh about 15% in my portfolio.

x x x

The investment in CBIP made up ~7.5% of my fund... Combine with TSH, the palm-oil related companies now weigh about 15% in my portfolio.

-- (End) --

.