This is a company that I had been observing since 2007, when it's still listed on MASDAQ. I bought 2000 units of it last month, at RM2.97, just before it plunge to the current level.

Main reason of buying is the high growing potential, supported by its great financial performance.

A review of historical data: (RM million)

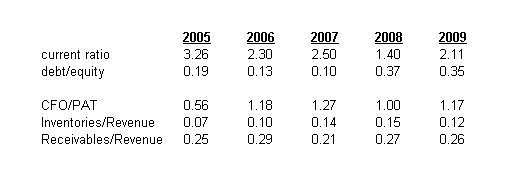

balance sheet ratios and cashflow:

In short summary:

- Good profit margin (maintaining above 20%)

- Great ROE (above 20%)

- High growth rate (25% CAGR for year 2004~2009)

- Healthy balance sheet and cashflow.

I think that Notion is able to maintain this performance in the next five years.

.

One more thing that I love Notion very much is the ability to diversified its product base. Below shows the product mix of Notion in recent years.

The balancing between SLR cameras and HDD sectors reduce Notion's dependency on a specific customer, hence lower its business risk.

This year 2010, the newly emerge customers, Samsung & Alphana, will bring Notion into the 2.5" HDD sector (producing baseplate and spindler motor hubs), hence further broadening its product base and customer base.

.

Recent development.

Soon after I bought Notion, its share price dip 40%.

Following the release of its latest quarterly report, we had learned that Notion is currently facing technical challenges, causing a high rejection-rate from its new customer, Samsung. The higher operating cost leads to a very poor profit margin.

In my opinion, the high-rejection-rates problem is just a temporarily issue. I have my confidence in Notion's management, and believe that the company will manage to get through this. (Though it may take months to fix the problem).

So, its current share price actually looks very attractive to me, and I'm currently considering to increase my stake in Notion.

.

No comments:

Post a Comment