Value Investing is an investment principle of "buying a stock with a price lower than its value". This is a conservative and secure investment strategy, and have been proven to be one of the highest-return strategy in long-run. (The followers of Benjamin Graham are able to achieve an average CAGR of 20% or higher.)

Graham's way of applying "Value-investing" principle is quite easy to follow. We just have to buy a company with a price below its net asset value. Applying the margin of safety concept, Graham prefer in buying a stock where its share price is lower than two-third (67%) of its net working capital. (In Graham's definition, net working capital = current asset - total liabilities.) And Graham encourage a widely diversified portfolio, in order to minimize the risk.

Later, affected by Philip Fisher's investment philosophy, Warren Buffett improved the "value-investing" strategy, by using a different technique in stock valuation. In stead of valuing a stock by its book asset value, Buffett calculate the "intrinsic value" of a stock, taking its earning power, brand-name, etc. into account. That's why Buffett always buy some companies which has very little assets but a strong earning power. Different from Graham, Buffett's portfolio is quite concentrated, normally less than 20 stocks. When Buffett found a good company, he can throw 20% of his money into it. (one of his record is investing about 40% of his funds into American Express.) He have a very good understanding on the companies he bought, thus the risk is minimized although the portfolio is not diversified.

Buffett said, "you need only a little margin of safety if you understand the business very well; but a high margin of safety is needed when you have limited knowledge about the business you bought." and he said, "I prefer to buy a wonderful company with a fair price, than a fair company with a wonderful price."

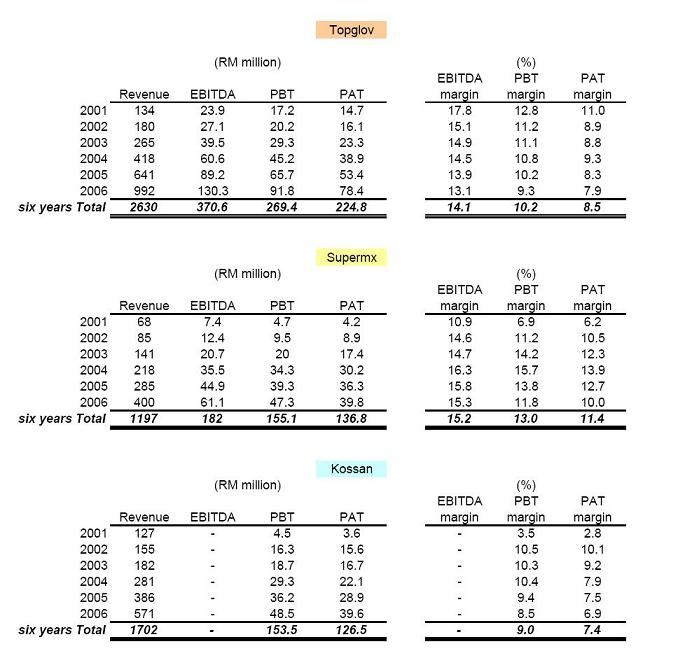

I prefer to learn the Buffett's way. But this require us to do a lots of study and research about the business of a company. I found that this is not an easy job. (You have seen the mistake I've made in selecting AirAsia). But I can learn a lots of knowledge during my research.

Sometimes, especially when I found that I've made a serious mistake, I wondered if I can understand a business as good as Buffett. Few months ago, I thought that I understand a company quite well; months later, I found that I was wrong either in the accounting calculation or about the industry's future prospect. When I was busy, I wondered is it a better choice if I start with Graham's way, which is much easier and lower risk, yet can generate a comparable return as Buffett's. I just need to do some financial calculating... not much research have to be done on the business nature of the companies. (while it is easy, it's very boring...)

The problem is, Graham's approach needs a fully diversified portfolio. Currently, my investment fund is only RM 25K. If I invest RM1000 into each stock, I can have 25 companies in my portfolio. But, from next year (2008) onwards, the minimum brokerage fee of buying/selling a stock (on-line) could be increased to RM28 (still a proposal now, waiting for approval from the authorities). If it becomes true, then the money I invested into each stock should be at least RM5000, just to limit my trading cost within 1%. Thus, I can only "diversified" my RM 25K into five stocks....

So... seems that I don't have a choice...